Understanding The Basics of TRID

Understanding The Basics of TRID

Have you heard of TRID and what it means to buy a home? TRID in real estate is something many are unfamiliar with.

Unless you work as a loan officer, chances are you are unfamiliar with the documents used when taking out a mortgage.

TRID stands for TILA-RESPA Integrated Disclosures. Knowing what you will sign to purchase a house is essential for potential home buyers.

Financial documents can be challenging to understand without training, but it is still advisable that you have a basic grasp of what to expect as you move forward with your loan.

The better educated you are about the process, the less intimidating the whole thing will be.

Working as a Southborough Real Estate agent, I often explain to buyers what they will sign when buying a home.

Essentially four documents will play a huge role in purchasing your home.

Learn what you can about these documents before you sign anything. The more you know, the more comfortable you will feel as you borrow money for your new property.

Let’s examine what TRID is and how it works when buying a house.

What is TRID in Real Estate

For homebuyers to become better purchasers of settlement services and eliminate kickbacks that increase the costs of settlement services, the government established what’s known as The Real Estate Settlement Procedures Act (RESPA) back in 1974.

This statute had become a staple in protecting consumers. Recently RESPA was updated.

On October 3, 2015, The Consumer Finance Protection Bureau, or CFPB for short, changed how the world of mortgage documents works in a real estate transaction.

This initiative is now known as The TILA-RESPA Integrated Disclosure Rule. Most people in the real estate industry refer to this as TRID. Without a doubt, TRID has significantly impacted the real estate industry. Many parties have been affected, including mortgage companies, real estate agents, attorneys for real estate, buyers, and sellers.

TRID was implemented to make it easier for consumers to understand the costs and fees they’ll face at closing.

TRID regulations specify what loan information lenders must give borrowers and when it must be provided. It also regulated what fees lender charge.

TRID aims to help educate borrowers on their mortgage options and ensure the lender has the consumer’s best interests at heart.

All mortgage lenders are required to follow TRID guidelines when they quote or issue mortgages. TRID was first introduced in 2010 by the Dodd-Frank Wall Street Reform Act and was approved in 2013.

If you will be buying a home shortly, educating yourself on TRID and how it will affect your home purchase is essential. Keep reading to learn about four crucial mortgage documents you will sign when buying a home.

4 Documents You Will Sign For Your Mortgage Under TRID

The Real Estate Settlement Procedures Act (RESPA) and the Truth in Lending Act (TILA) have been put in place by legislators to protect home buyers from hidden fees and other abuses by real estate agents, lenders, and title companies.

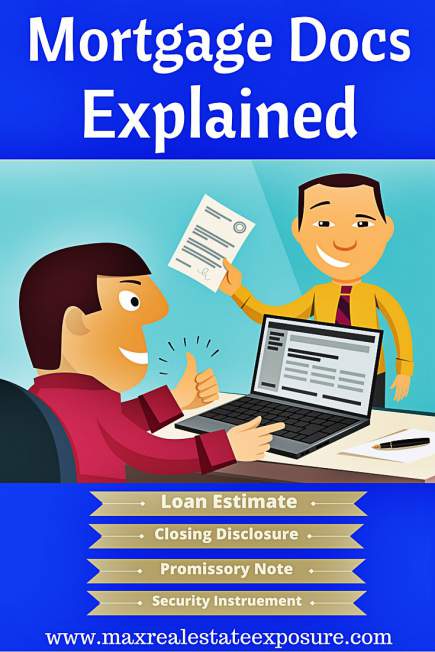

As of October 2015, the Consumer Financial Protection Bureau (CFPB) condensed the various fee disclosures and mortgage rate documents into two standardized forms. These forms – the Loan Estimate and the Closing Disclosure – along with the promissory Note and the security instrument- will play a significant part in your loan process.

The loan documents buyers have to deal with have been simplified somewhat over previous years, so you will have an easier time understanding the loan you are taking out.

These forms should be reviewed carefully as you receive them to ensure they match your expectations and what the seller and the lender told you.

1. Loan Estimate

The Loan Estimate is a document that details your loan terms, including the projected payments and the line item closing costs.

The Loan Estimate is a document that details your loan terms, including the projected payments and the line item closing costs.

You are supposed to get the Loan Estimate within three days after you apply for a loan.

Review the Loan Estimate carefully to ensure you understand exactly what the loan will entail and that you are comfortable with the terms.

Some of the big mistakes that some borrowers make are shopping for the best mortgage interest rate without understanding how other costs factor into precisely what they are paying.

For example, you might find a mortgage lender who will give you a lower interest rate than another, but if you pay more points and closing costs to get that rate, you might not get the best deal.

This is how some borrowers end up paying too much for their mortgage. Instead of shopping for the lowest rate, homebuyers should look at the entire package and all the program costs.

2. Closing Disclosure

The Closing Disclosure will look very similar to the Loan Estimate. It includes information on the loan terms while also adding a detailed list of paid by who – buyer, seller, and third parties.

Here you will find all the costs associated with the sale and who is covering those costs, which is essential if you want to ensure everyone is doing what was agreed.

The Closing Disclosure is supposed to be delivered to you three days before the closing of the sale.

3. The Promissory Note

Here is the actual loan contract. The Promissory Note will list all the loan details, including the length of time, interest rate, payment intervals, early payment penalties, and all other information pertaining to the loan.

The Note will also state that you are putting up the home as collateral on the loan. If you cannot meet the loan terms, the Note says that your lender can take back the house as payment for what is owed.

4. The Security Instrument

Depending on your state, the loan will require you to sign a mortgage or a deed of trust. Both documents are there to pledge the home as security for the loan.

The document will also define how the home will be occupied, either an owner-occupied, second home or non-owner occupied. Each of these requires that you use the house in a certain way.

Owner-occupied means you must live in the home as your primary residence for at least a year before you try to rent or use it as a second home.

If the home is defined as a second home, you must use it as one – not a primary residence, nor a rental.

Lastly, the non-owner occupied designation states you can rent the home. This category comes at a higher cost; if the house is non-owner occupied, you can always change it to one of the other two categories.

Any Problems With TRID in Real Estate?

One might wonder if putting TRID in place has caused any industry issues. The answer would be yes, it has.

One might wonder if putting TRID in place has caused any industry issues. The answer would be yes, it has.

One of the biggest complaints so far is the time it has added to complete the mortgage process and, ultimately, the time it takes to close a home.

A number have gone on record saying that it has done more harm than good, including Governor and former Presidential candidate Chris Christie quoted on Housing Wire. Chris states he would deregulate the consumer protection bureau and roll back some recent initiatives if elected. He also mentioned that TRID was another example of the government creating more problems than it solves.

Another TRID-related problem that has been in the news recently is investors refuse to buy certain loans because they are not compliant.

ClosingCorp, a company that operates the premier source of intelligence for closing costs and service providers in the U.S. residential real estate industry, recently reported that 63 percent of buyers said that the new “Know Before You Owe” forms for loan estimates and closing disclosures are easier to understand than the old documents that were used. This was based on a survey of 1000 respondents.

Additionally, 68 percent said the new forms did a better job preparing them for the closing costs they would have to pay. 6 percent thought otherwise.

Another 65 percent of the respondents said that the costs and fees were “explained better” in their most recent home-buying experience. It seems that TRID in real estate sales has been working just fine.

In my experience as a Realtor, I have not noticed any significant issues with TRID for real estate since it was implemented. It has been business as usual.

What Are The Exact TRID in Real Estate Rules and Guidelines?

Let’s examine the TRID rules.

- No more application fees: Under TRID guidelines, a lender cannot charge fees before offering a Loan Estimate. A credit report fee is the only expense a mortgage lender can charge.

- Fast delivery of the Loan Estimate: Mortgage lenders must issue a Loan Estimate within three days after receiving a borrower’s application. This ensures buyers time to ask the lender any additional questions they need answering.

- Disclosures and estimates kept on file: Lenders must keep a copy of your Loan Estimate at least three years after signing your mortgage. The closing disclosure is for at least five years after you sign your mortgage.

- A 3-day waiting period for your Closing Disclosure: Mortgage lenders must provide your Closing Disclosure at least three business days before signing the mortgage. If there are requested changes to your Closing Disclosure, the lender is required to provide you with a new contract. You must also wait an additional three business days until the finalization of the loan.

- Contact information is a requirement: Lenders must provide their contact information and a way to reach the loan officer in the Loan Estimate.

Educate Yourself on TRID in Real Estate For Maximum Confidence

The home-buying process can move along quickly once things get going, so the time to educate yourself about the loan process is before you purchase.

A home is a significant purchase – often the most critical purchase people make. Whibeing be a little nervous about such a big commitment is normal. You can lessen the anxiety by ensuring you have a basic grasp of the buying process. Millennial homebuyers face real estate changes that other first-time homebuyers have not experienced.

Working With Your Realtor And Lender

Your biggest ally in the buying process is your real estate agent. It is advisable to talk to your agent before you make an offer to get all the available advice and insight about what is coming up.

I highly recommend you understand all the things to do before buying a home. A real estate agent can be your greatest ally, but only if they are a true professional. Keep in mind just about anyone can get a real estate license!

Your real estate agent should be able to tell you about the basics of the loan process and how to navigate it. You can also make sure you pick a lender you are comfortable with and ask your mortgage broker to explain the loan process and what your part will be in it. They can talk you through the forms that will be coming up and give you an idea of what to pay attention to.

Some of the biggest mistakes for first-time buyers are financial ones. Getting into financial trouble is the last thing you want as a new homeowner, as it can follow you for years.

Feeling a little out of your element is expected when taking out a mortgage. It is not every day that most people buy a home. A home loan involves a lot of money and a complicated process, sometimes baffling to those not trained.

Final Thoughts About TRID

Fortunately, just like so many other home buyers, you can learn the basics and trust your partners, like your real estate agent, to help you make sure that you are doing what is in your best interests.

Hopefully, you now have a better understanding of the TRID regulations.

Additional Helpful Mortgage and Home Buying Articles

- What is the best mortgage for my needs – how can you tell you’re getting the best mortgage? Get some helpful guidance in these valuable resources.

- How does a buyer use a right of first refusal in real estate – get helpful guidance that covers everything you need to know about the first right of refusal.

- Negotiating tips for home buyers – learn some better-negotiating tactics when making your first home purchase.

- How to know the right offer for a home – discover how to evaluate an offer so you make the best decision possible.

When buying a home for the first time, you must educate yourself. Use these additional home-buying resources to make intelligent decisions when purchasing a home for the first time.

Hopefully, you are now somewhat familiar with the TRID mortgage documents you must sign!

About the Author: The above Real Estate information on what TRID is in Real Estate was provided by Bill Gassett, a Nationally recognized leader in his field. Bill can be reached via email at billgassett@remaxexec.com or by phone at 508-625-0191. Bill has helped people move in and out of Metrowest towns for the last 37+ Years.

Are you thinking of selling your home? I am passionate about Real Estate and love sharing my marketing expertise!

I service Real Estate Sales in the following Metrowest MA towns: Ashland, Bellingham, Douglas, Framingham, Franklin, Grafton, Holliston, Hopkinton, Hopedale, Medway, Mendon, Milford, Millbury, Millville, Northborough, Northbridge, Shrewsbury, Southborough, Sutton, Wayland, Westborough, Whitinsville, Worcester, Upton, and Uxbridge MA.